It is important to know your credit score in order to maintain good credit. You can check your score for free every four months or once a year. Credit card companies often offer free FICO score reporting. It is a good idea also to check your credit score at minimum three times per year.

Credit score can be affected with hard inquiries

While you may not realize it, hard inquiries can negatively impact your credit score. When a creditor requests your credit report, it can lead to a negative impact on your credit score. These inquiries are usually the result of identity theft or error and you might not notice them until there is a large number. Routine monitoring your credit report can help identify errors. You can send a dispute correspondence to the credit bureau if you find an error. You can also contact your lender to dispute the inquiry and report fraud to the Federal Trade Commission.

Generally, a hard inquiry can lower your score by one to five points. The exact amount will depend on the credit score you have and how long ago it has been since your previous inquiry. It is best to avoid making too many inquiries unless you absolutely need them.

In determining your credit score, the most important factor is making timely payments

When making your payments on time is an important factor in determining your credit score. Paying on time is crucial because late payments could make your debt more expensive and compound. Another factor is your credit utilization relative to your total debt. Lenders are not happy when you have high credit debts. It is therefore important to keep your credit utilization under 30 percent. Your credit score can be improved by paying off your existing credit cards and avoiding new ones.

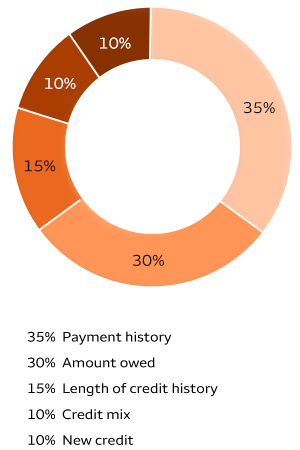

Your payment history is responsible for 35% your overall credit score. This information reveals if you have paid your bills on time and if you have missed payments. This information is used by lenders to assess your ability to repay your debts on a timely basis. Late payments can harm your credit score. However you'll have a longer payment history which will help your score.

Correct inaccurate credit information

If you believe there is incorrect information on your credit report, dispute it with the credit bureaus. They must examine the error and provide you with a copy of your credit reports. The bureau might not be able to agree with your complaint so it will remain on the credit report. You can correct the error by contacting the creditor and asking for clarification. Or, you can re-dispute your complaint with additional information.

You can dispute inaccurate information by writing a dispute letters. It should contain a dispute document and copies supporting documentation. Send your dispute letter to the credit reporting company, using the dispute address on the credit report. It should be sent by certified mail and accompanied with a return receipt.

False information on your credit reports can adversely impact your credit score. It can also affect your ability of borrowing money or getting credit cards. While it is easy, the outcome can prove frustrating. But it's worth it if you can get an accurate report.